Stocks, Tweets, and Volatility

INFO 2950

5/5/23

Visualization of Number of Tweets’ Effect on Volatility

Our first inference model was to find the number of tweets and their affect on the volatility on a selection of stocks across market caps.

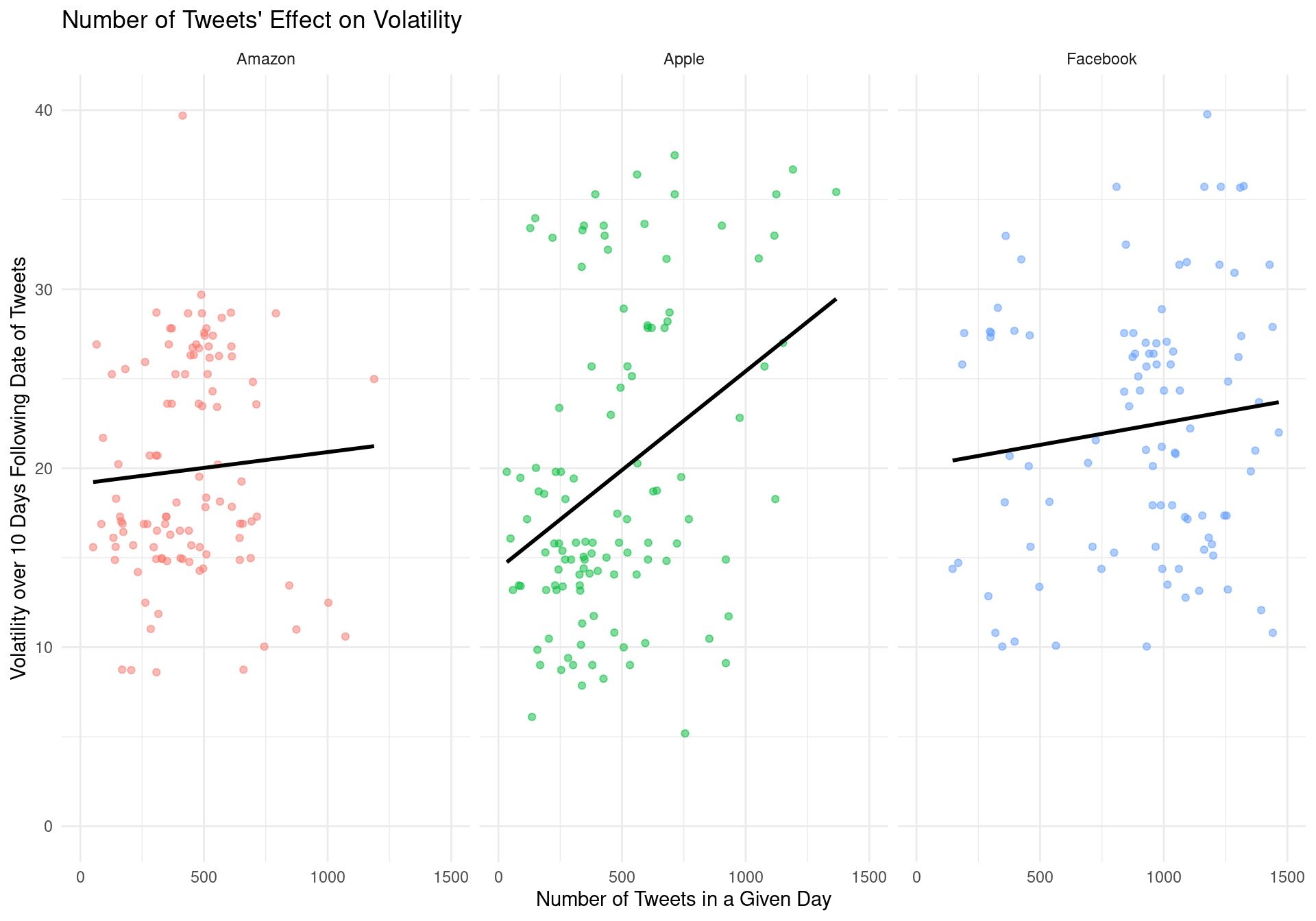

The first visualization below is specific to Facebook, Apple and Amazon. Companies apart of FAANG and generally in the upper echelon of market caps

Continued

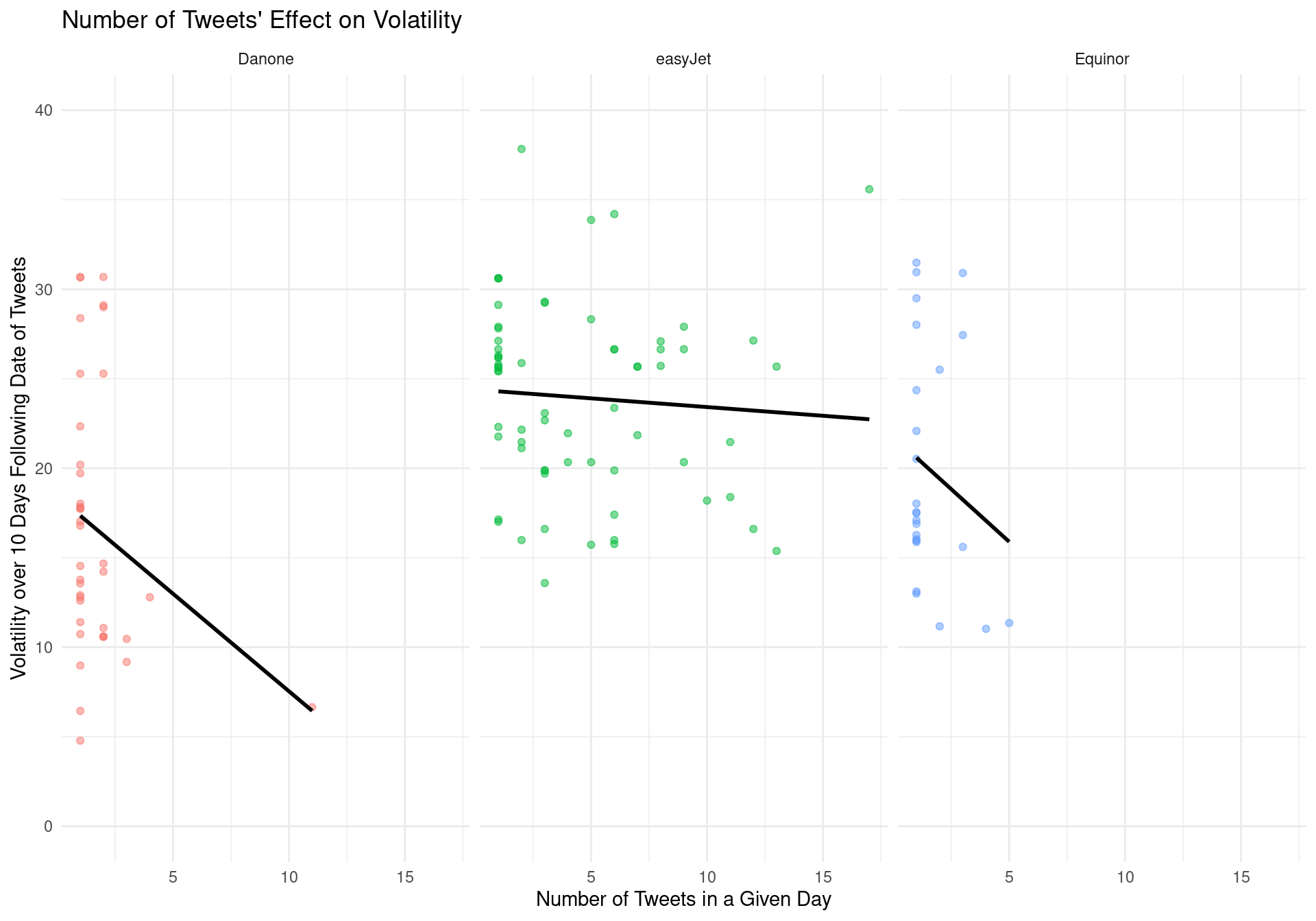

The second visualization below is specific to easyJet, Danone and Equinor. Companies with significantly smaller market caps then the previously mentioned companies.

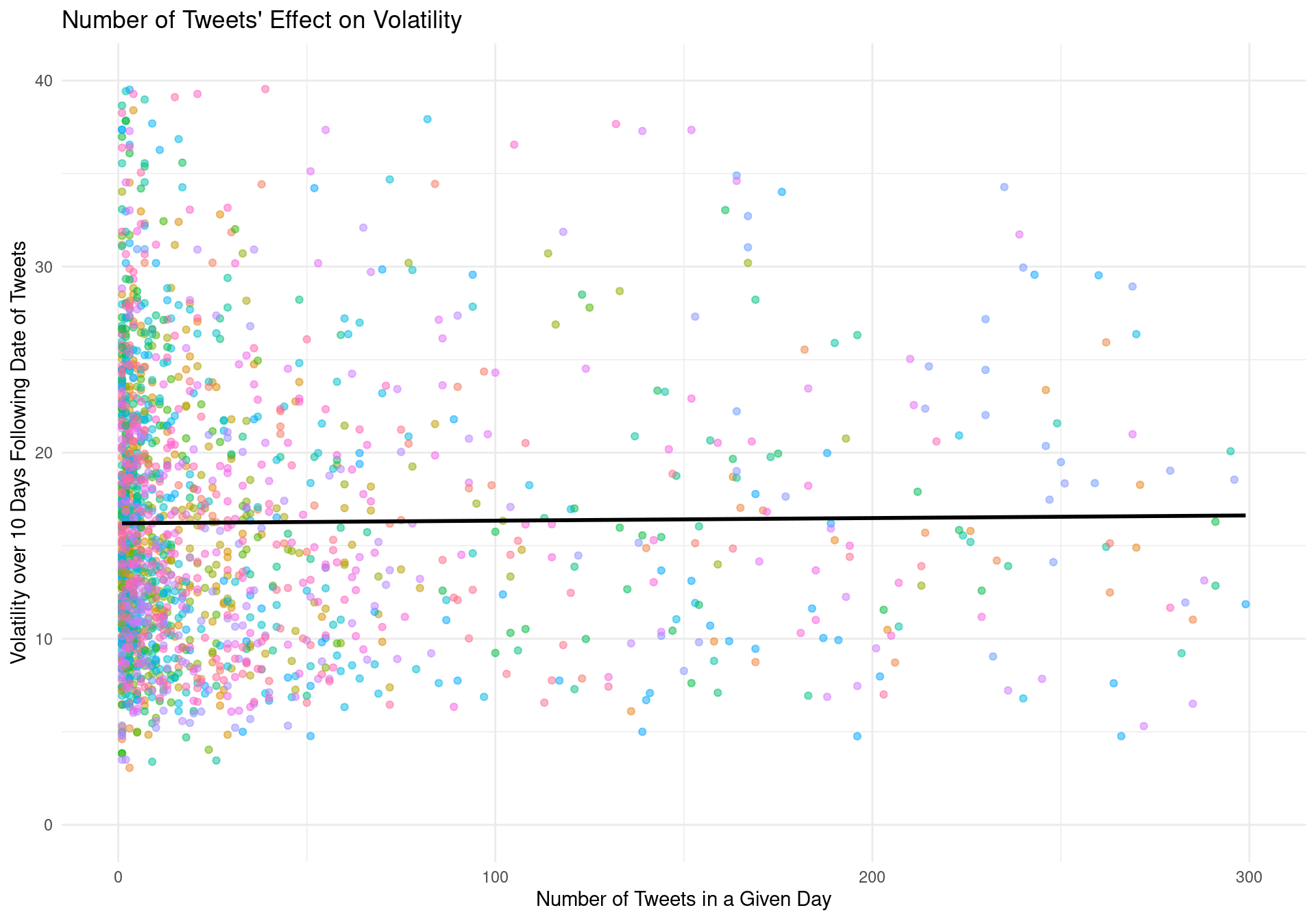

Number of Tweets’ Effect on General Stock Volatility

\[ volatility = 18.35 + 0.00002 \times number~of~tweets \]

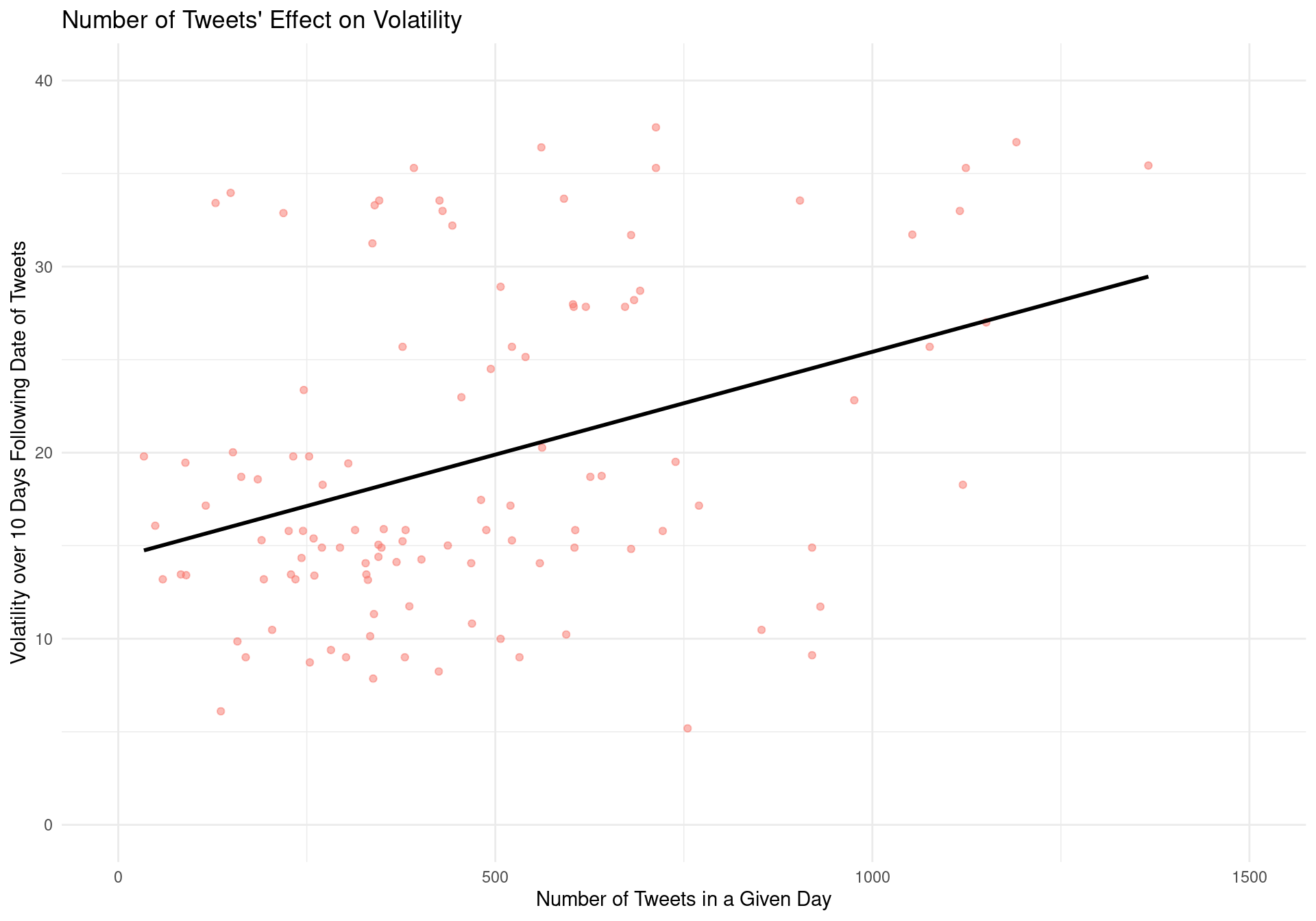

Number of Tweets’ Effect on Apple’s Volatility

# A tibble: 2 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 17.5 1.30 13.5 9.62e-26

2 tweet_num 0.00607 0.00189 3.21 1.68e- 3\[ volatility = 17.78 + 0.00568 \times number~of~tweets \]

Tweet Sentiment’s Impact on Stock Price

# A tibble: 1 × 1

p_value

<dbl>

1 0.986

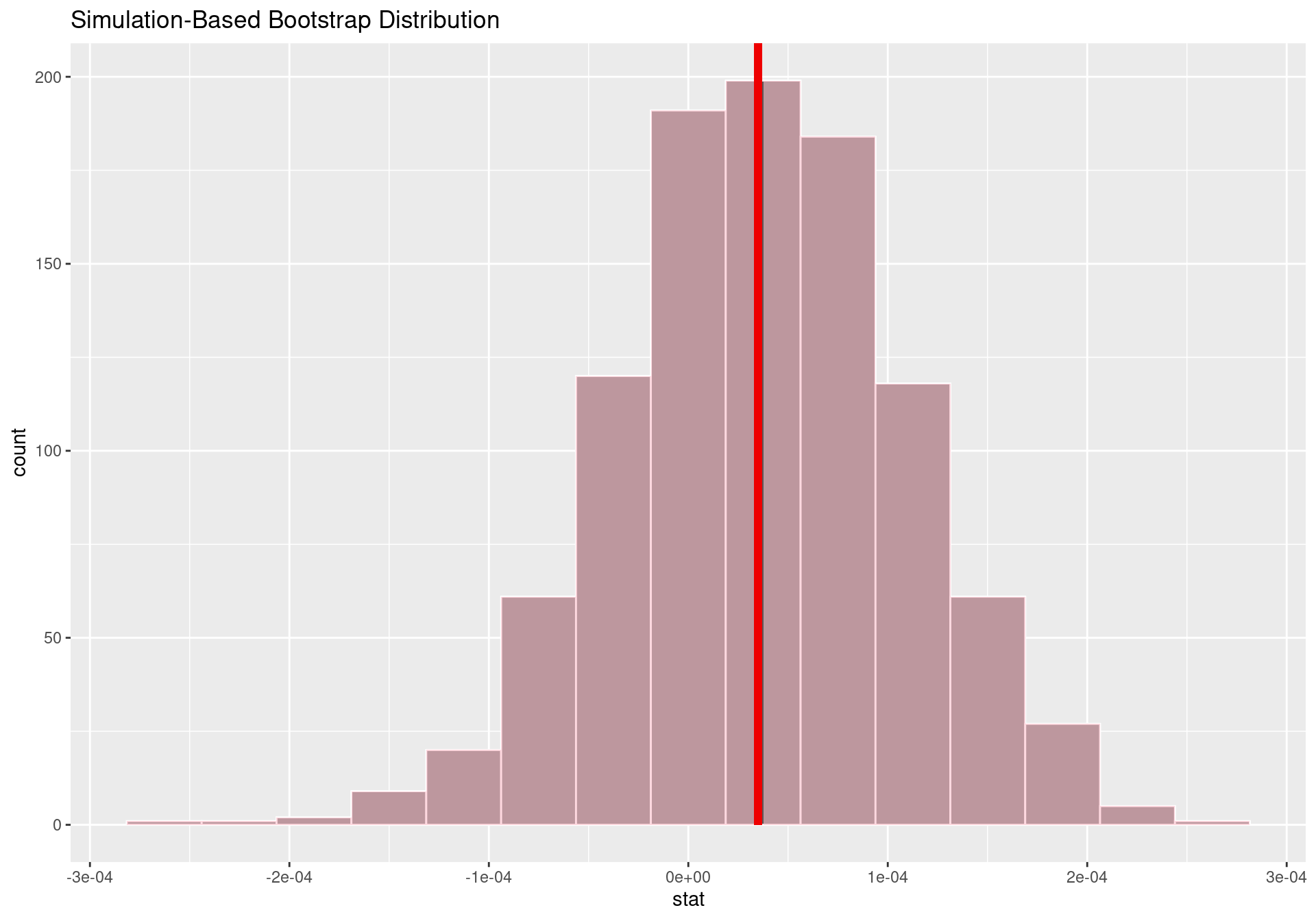

With a P-value is .986, we fail to reject the null hypothesis. The null hypothesis remains true

Our findings indicate that there is no difference of 1 day changes in stock prices for stocks based on tweets mentioning them